PRINCIPLES OF ECONOMICS

INTRODUCTION TO THE PRINCIPLES OF ECONOMIC

Political Economy or Economics is a study of mankind in the ordinary business of life; it examines that part of individual and social action which is most closely connected with the attainment and with the use of the material requisites of wellbeing.

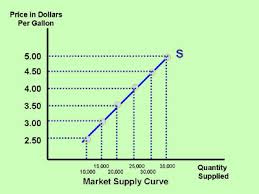

3. Supply

3.3. supply curve

The law of supply is based on the following assumptions:

Producers are profit-maximizing: Producers want to maximize their profits, and they will produce more of a good if the price is high enough to cover their costs and earn a profit.

The cost of production is constant: The cost of producing a good does not change as the quantity produced increases.

There are no changes in technology: New technologies can change the cost of production, but the law of supply assumes that technology remains constant.

There are no changes in the number of producers: The number of producers in the market does not change.